I spent the early part of this week at Salesforce.com’s annual Dreamforce conference. Here are my observations.

The big news was for geeks. The main theme of the conference was Salesforce1, a new set of technologies that make it vastly easier to deliver and integrate mobile versions of Salesforce-based applications. It is apparently a major technical accomplishment and at least one of my technical friends was hugely impressed. But I can’t say I personally found it all that exciting. Perhaps we’ve reached the point where we expect technology to do pretty much everything, so the line between what's already available and what's new is only visible to experts. Any way you slice it, focusing on platform technology is much less exciting than last year's vision of "social enterprise".

The bad news was for B2B marketing automation. Conference presentations confirmed that Pardot, the B2B marketing automation system that Salesforce acquired as part of its ExactTarget acquisition, has been separated from the rest of ExactTarget and made part of the Sales cloud. There, Pardot is described only as providing lead scoring and nurture programs, which ignores landing pages, behavior tracking, and other features that B2B marketing automation usually provides (and Pardot includes). In terms of infrastructure, Pardot will eventually work directly from the CRM data objects, rather than maintaining its own synchronized database. (Data outside the CRM structure, such as detailed Web behaviors, will remain separate.)

What this means is that Salesforce sees B2B marketing automation as just an appendage of sales automation. This is pretty much the same constricted view of marketing automation that Salesforce management has held all along. The logical consequence is to make lead scoring and nurture campaigns standard features within the Sales offering and discard Pardot as a separate product. I should stress that no one at Salesforce said this was their plan, but it seems inevitable. If and when that does happen, only the most demanding companies will purchase a separate B2B marketing automation product.

To put a more optimistic spin on the same news: Salesforce will continue to let independent B2B marketing automation apps synch with Sales. If Salesforce does merge Pardot features into its core Sales product, then marketers who have a more expansive view of B2B marketing automation functions (or who simply want a system of their own) will be forced to buy from someone else.

The interesting news was that B2C marketing automation remains separate. Salesforce’s list of business groups includes the Sales Cloud, Service Cloud, and ExactTarget Marketing Cloud. Did you notice that just one of these has its own brand? As this suggests, and conference presentations confirm, Salesforce has kept B2C marketing distinct from its Sales and Service businesses, most importantly at the data and platform levels. The ExactTarget Marketing Cloud does now include Salesforce’s previously-purchased social marketing components, Radian6 social monitoring and Social.com social advertising. It also includes the iGoDigital predictive personalization technology that came along with the ExactTarget acquisition.

Salesforce did announce some plans to integrate the Marketing cloud with Sales and Service, but they are pretty much arm’s length: Marketing can receive alerts about changes in Sales (and I assume Service) data, even though that data remains separate; Sales and Service can send emails through the ExactTarget engine; Sales and Service can receive content recommendations from the Marketing predictive modeling tool. As near as I can tell, this is the same type of API-level integration available with any third-party system. For what it’s worth, the ExactTarget Marketing Cloud APIs are also part of Salesforce1, but don’t confuse that with sharing the same underlying platform.They don't.

The good news is the B2C marketing vision. It’s not really surprising that Salesforce kept its B2C platform separate, since Salesforce's core technology isn’t engineered for the massive data volumes and analytical processing needed for B2C in general and consumer Web marketing in particular. Happily, this technical necessity is accompanied by what strikes me as a sound vision for customer management. ExactTarget framed this around three goals: single view of the customer; managing the customer journey; and personalized content across all channels and devices. It described major features for each of these: a unified metadata layer to access (and optionally import) data from all sources; a “customer journey” engine to manage multi-step, branching flows; and predictive modeling to select the best offers and contents across email and Web messages.

This felt like a more coherent approach than Salesforce described for the Sales cloud, where external data and predictive modeling in particular were barely mentioned (or, more precisely, are still being left to App Exchange partners). The ExactTarget cloud still lacks tools to associate customer identities across email, phone, postal, social, and other systems, although there are plenty of partners to provide them. I didn’t get a close look at the details of the ExactTarget functions, which will really determine how well it competes with other customer management platforms. But the general approach makes sense.

News of the revolution may be exaggerated. Salesforce argued during the AppExchange Partner keynote that the AppExchange and Salesforce platform have created a “golden age of enterprise apps” by enabling small software developers to sell to big enterprises. One part of the argument is that the platform itself lets small vendors break through the credibility and scalability barriers that have historically protected large enterprise software vendors. The other is that end-users can purchase and deploy apps without involving the traditional gatekeepers in enterprise IT departments. A corollary to this is that end-users have different priorities than IT buyers – in particular, end users care more about ease of use – so successful software will be different.

Of course, this is exactly what the AppExchange partners wanted to hear and exactly the strategy behind Salesforce’s platform approach in the first place. But that doesn’t necessarily make it untrue: and, if correct, it would indeed be a revolution in the enterprise software industry.

But some revolutions are bigger than others. Even in an app-based world, individual users won't be making personal decisions about how to run core business processes. Rather, systems will be chosen at the department level because companies can more or less safely assume that whatever the department chooses will integrate smoothly with the corporate backbone. That's certainly a change but bear in mind that departmental buyers will have the same preference as corporate IT groups for working with the smallest possible number of vendors. This means there will still be the familiar tendency for individual vendors to add more functions over time. So industry dynamics may change less than you’d expect.

Showing posts with label pardot. Show all posts

Showing posts with label pardot. Show all posts

Friday, November 22, 2013

Thursday, August 23, 2012

Raab Report: Act-On, Eloqua, Pardot, and Marketo Vie to Lead in Mid-Size B2B Marketing Automation Segment

Today I’ll present the third and (mercifully?) final installment in my series of posts on leaders in the different B2B marketing automation sectors, as determined by the ratings in our VEST report. I’ve saved the best for last, in the sense that the small to mid-size sector is the heart of the industry and its most complicated arena.

We define small to mid-size business as companies with $5 million to $500 million revenue. This covers a broad range of marketing users with widely varied needs. Most require the full set of marketing automation functions but apply these in simple ways. They have one to fifteen marketing automation users. This sector generates nearly 60% of 2012 revenue ($200 million) from 33% of the installations (9,400 as of mid-2012). The VEST report provides separate client counts for small business ($5 million to $20 million revenue) and mid-size business ($20 million to $500 million). These account for 16% and 41% of revenue and 16% and 17% of installations, respectively. Although small businesses generally buy lower-priced systems, they have largely the same requirements as mid-size companies.

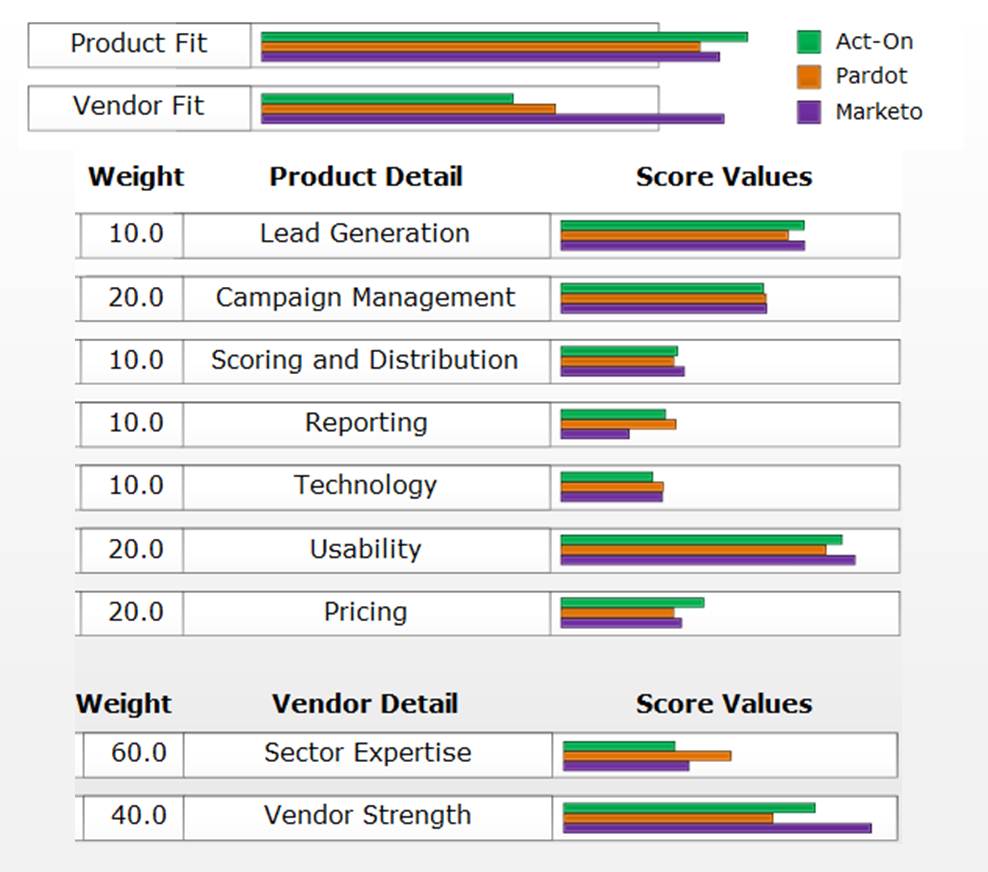

The leaders quadrant in this sector is quite crowded, with Act-On, Eloqua, Pardot, and Marketo all jostling for position. Silverpop, Neolane, and Genius are all lurking nearby. In case you haven’t caught on to my color coding, blue type indicates that Eloqua and Neolane are leaders in the large company segment, while red type shows the others have their strongest position in this sector.

The variety of users within this segment is reflected by the differences among the leaders. Act-On, Pardot, and Genius specialize in smaller companies than Marketo or Silverpop, which in turn serve generally smaller clients than Eloqua or Neolane. Act-On’s position on top of the product fit range is a bit misleading: when you look at the components of that score (see below; this comparison chart is another VEST feature), the vendors are all very close. In fact, the only category where Act-On scores higher than everyone else is pricing.

This isn’t at all to say that the products are equivalent. Rather, it means they each have different strengths and weaknesses that balance each other out when measured with generic scoring weights. For actual buyers with clear priorities, the difference among these vendors’ scores will almost always be much larger.

As with the other sector charts, the vendors in the upper left are also worth considering: they have strong product fit but relatively low market position. SalesFusion appears here as it did in the micro- and large-business charts: what can I say, they have rich features at a good price. (And, no, they’re not my client.) eTrigue is the other noteworthy contender; it and LeadFormix are both close to the leader quadrant based on their vendor fit.

If there’s any one lesson from all these charts, it’s that picking the “leading” vendor is no guarantee of making a good choice. Our three sets of weights yield different sets of leaders, and even those vendors have different strengths and weaknesses. I’ve said it a million times but I’ll say it again: there’s no substitute for understanding your own needs and finding out which vendors match them best.

We define small to mid-size business as companies with $5 million to $500 million revenue. This covers a broad range of marketing users with widely varied needs. Most require the full set of marketing automation functions but apply these in simple ways. They have one to fifteen marketing automation users. This sector generates nearly 60% of 2012 revenue ($200 million) from 33% of the installations (9,400 as of mid-2012). The VEST report provides separate client counts for small business ($5 million to $20 million revenue) and mid-size business ($20 million to $500 million). These account for 16% and 41% of revenue and 16% and 17% of installations, respectively. Although small businesses generally buy lower-priced systems, they have largely the same requirements as mid-size companies.

The leaders quadrant in this sector is quite crowded, with Act-On, Eloqua, Pardot, and Marketo all jostling for position. Silverpop, Neolane, and Genius are all lurking nearby. In case you haven’t caught on to my color coding, blue type indicates that Eloqua and Neolane are leaders in the large company segment, while red type shows the others have their strongest position in this sector.

The variety of users within this segment is reflected by the differences among the leaders. Act-On, Pardot, and Genius specialize in smaller companies than Marketo or Silverpop, which in turn serve generally smaller clients than Eloqua or Neolane. Act-On’s position on top of the product fit range is a bit misleading: when you look at the components of that score (see below; this comparison chart is another VEST feature), the vendors are all very close. In fact, the only category where Act-On scores higher than everyone else is pricing.

This isn’t at all to say that the products are equivalent. Rather, it means they each have different strengths and weaknesses that balance each other out when measured with generic scoring weights. For actual buyers with clear priorities, the difference among these vendors’ scores will almost always be much larger.

As with the other sector charts, the vendors in the upper left are also worth considering: they have strong product fit but relatively low market position. SalesFusion appears here as it did in the micro- and large-business charts: what can I say, they have rich features at a good price. (And, no, they’re not my client.) eTrigue is the other noteworthy contender; it and LeadFormix are both close to the leader quadrant based on their vendor fit.

If there’s any one lesson from all these charts, it’s that picking the “leading” vendor is no guarantee of making a good choice. Our three sets of weights yield different sets of leaders, and even those vendors have different strengths and weaknesses. I’ve said it a million times but I’ll say it again: there’s no substitute for understanding your own needs and finding out which vendors match them best.

Wednesday, June 27, 2012

Dell To Resell Pardot Marketing Automation

Dell announced today that it has added Pardot marketing automation to its list of Dell Cloud Business Software applications. Other products in the suite include Salesforce.com for sales automation and customer service, Adobe EchoSign for e-signatures, AppExtremes Conga Composer for proposal creation, Dell’s own Boomi for application integration, and a Dell-built analytics platform. That is some pretty good company to keep.

Beyond the Pardot system itself, the Dell offering includes pre-built integration with the other Dell products and with Microsoft Dynamics CRM, and fixed-price implementation packages (from free to $5,000) including training, campaign development, site search setup, CRM integration, and Google AdWords integration. The Pardot system costs from $1,000 to $3,000 per month depending on the email volume, file size, and numbers of forms, landing pages, programs, and automation rules. This is the same as Pardot’s direct-sold prices. Dell also offers a 30 day free trial of Pardot.

The details of the deal are probably less important than its potential for market penetration. Dell hasn’t been on my list of potential entrants into the marketing automation space, but it certainly has a huge presence among small and mid-size businesses. This gives it the capability to add thousands of clients to Pardot’s existing base, which has just recently passed 1,000. Like Intuit’s acquisition last month of local marketing vendor Demandforce, a well-executed rollout could quickly establish a firm whose market share dwarfs existing competitors. In some ways, the Dell/Pardot deal is even more interesting than Intuit/Demandforce, because it touches the small to mid-size businesses that form the core of the B2B marketing automation client base. Intuit/Demandforce will serve many micro-businesses, while other recent deals (FICO/Entiera and Experian/Conversen) are aimed at larger, business-to-consumer marketers.

This doesn't mean an effective Dell/Pardot rollout is guaranteed. These sorts of relationships often fizzle quickly, typically because the larger company’s sales force can’t be bothered to sell the new partner’s product. That seems a bit less likely to happen in this case, since Dell’s cloud business group offers just a handful of applications and Dell has traditionally been a very effective marketer – although its recent performance has been spotty.

Whatever the result of this particular deal, it is more evidence that the B2B marketing automation industry is rapidly approaching consolidation. As deep-pocketed outside companies become active, they battle each other on a grand scale and little firms get crushed almost accidentally. It may be some time before a single victor emerges – if ever – but it’s hard to imagine many of today’s small companies remaining successful as elephants stampede all around them.

Tuesday, October 11, 2011

Marketo Spark Targets Small Business Marketing Automation

Marketo today announced the launch of Spark, a new brand aimed at small and mid-size business. Functionally, Spark is pretty much identical to the standard Marketo system. Exceptions are advanced features including revenue cycle reporting, email deliverability assistance, API access, fine-grained user rights management, and the Sales Insight salesperson application. Most of these aren’t of interest to small business, and several involve additional charges even for Marketo’s regular packages.

So the news here is price. Spark starts at $750 per month with no annual contract, compared with Marketo’s $2,000 per month minimum and annual contract for its full-featured Professional Edition. Marketo has discontinued its $1,200 per month Small Business Edition, which lacked some features now included with Spark.

In other words, this is a price cut. To me, it looks like a reaction to the success of other low cost small business systems, including HubSpot, Act-On Software, and Pardot. (HubSpot and Act-On have similar pricing to Spark, while Pardot runs a bit higher.) Some of those firms are actually growing at a faster rate than Marketo, although on a smaller base. Spark should help to blunt their momentum while increasing Marketo's own client total -- a closely watched metric, regardless of the associated revenue per client.

Whether Marketo actually makes any money at Spark's price is questionable. It really depends on the sales and support costs, and Marketo doesn’t appear to have changed how those are delivered to keep them down. Other small business specialists have designed sales and support models that are not as staff-intensive as traditional approaches. By contrast, Marketo is stressing that Spark includes services to help clients take advantage of their systems.

Of course, Marketo could have lowered its entry price without creating a new brand. So why bother to launch Spark?

One reason may be to avoid cannibalizing sales of its other, higher-priced editions. But, let’s face it, any sentient buyer will notice that Spark is out there. I think the more important reason is that Spark lets Marketo address small businesses separately from larger companies. The two groups do have different needs and neither wants a system designed for the other. Spark lets Marketo position itself as a small business specialist when selling to small businesses, without alienating big-business marketers who would consider a small business system an unsuitable toy.

This is a delicate game. For one thing, "small business" means different things to different people. Small business specialists like Infusionsoft and OfficeAutoPilot actually serve a different market -- one that I label "microbusiness" and put at under $5 million revenue. Those products have a different configuration from Spark, HubSpot, Pardot, or Act-On. Specifically, Infusionsoft and OfficeAutoPilot have starting prices around $300 per month and offer built-in shopping carts and CRM. (Other micro-business specialists like Genoo and MakesBridge also have a sub-$500 monthly price, but no CRM or shopping.) Although Spark is not aimed at the micro-business market, some people may not recognize the distinction.

Nor it is clear that the Spark brand will be enough let Marketo play in both the small and mid-size business segments ($5 to $500 million revenue, by my definition) and the big business segment (more than $500 million revenue.) Nearly every other marketing automation vendor focuses on one or the other. The main exception is HubSpot, which is also trying to add larger clients without losing its small business base -- and facing some positioning challenges of its own.

Spark also poses a financial challenge. Marketo has said it will earn around $30 million revenue in 2011, and will have an average of around 1,100 clients. That comes to about $2,500 per client per month, a figure Marketo has been striving to increase. A large number of Spark clients at $750 per month would dramatically reduce its average. The profit margins, if any, will surely be lower as well, again dragging down the corporate average.

Now, this is all interesting stuff, but does it matter to anyone who isn't a Marketo investor? Probably not. Spark may push prices a little lower and may put a small crimp in some competitors' growth rates. It may also give small business marketers another fine set of resource materials to complement those from HubSpot and others. But the bottom line is that similar capabilities were already available at a similar price point from Marketo and others. Spark just doesn't change much.

So the news here is price. Spark starts at $750 per month with no annual contract, compared with Marketo’s $2,000 per month minimum and annual contract for its full-featured Professional Edition. Marketo has discontinued its $1,200 per month Small Business Edition, which lacked some features now included with Spark.

In other words, this is a price cut. To me, it looks like a reaction to the success of other low cost small business systems, including HubSpot, Act-On Software, and Pardot. (HubSpot and Act-On have similar pricing to Spark, while Pardot runs a bit higher.) Some of those firms are actually growing at a faster rate than Marketo, although on a smaller base. Spark should help to blunt their momentum while increasing Marketo's own client total -- a closely watched metric, regardless of the associated revenue per client.

Whether Marketo actually makes any money at Spark's price is questionable. It really depends on the sales and support costs, and Marketo doesn’t appear to have changed how those are delivered to keep them down. Other small business specialists have designed sales and support models that are not as staff-intensive as traditional approaches. By contrast, Marketo is stressing that Spark includes services to help clients take advantage of their systems.

Of course, Marketo could have lowered its entry price without creating a new brand. So why bother to launch Spark?

One reason may be to avoid cannibalizing sales of its other, higher-priced editions. But, let’s face it, any sentient buyer will notice that Spark is out there. I think the more important reason is that Spark lets Marketo address small businesses separately from larger companies. The two groups do have different needs and neither wants a system designed for the other. Spark lets Marketo position itself as a small business specialist when selling to small businesses, without alienating big-business marketers who would consider a small business system an unsuitable toy.

This is a delicate game. For one thing, "small business" means different things to different people. Small business specialists like Infusionsoft and OfficeAutoPilot actually serve a different market -- one that I label "microbusiness" and put at under $5 million revenue. Those products have a different configuration from Spark, HubSpot, Pardot, or Act-On. Specifically, Infusionsoft and OfficeAutoPilot have starting prices around $300 per month and offer built-in shopping carts and CRM. (Other micro-business specialists like Genoo and MakesBridge also have a sub-$500 monthly price, but no CRM or shopping.) Although Spark is not aimed at the micro-business market, some people may not recognize the distinction.

Nor it is clear that the Spark brand will be enough let Marketo play in both the small and mid-size business segments ($5 to $500 million revenue, by my definition) and the big business segment (more than $500 million revenue.) Nearly every other marketing automation vendor focuses on one or the other. The main exception is HubSpot, which is also trying to add larger clients without losing its small business base -- and facing some positioning challenges of its own.

Spark also poses a financial challenge. Marketo has said it will earn around $30 million revenue in 2011, and will have an average of around 1,100 clients. That comes to about $2,500 per client per month, a figure Marketo has been striving to increase. A large number of Spark clients at $750 per month would dramatically reduce its average. The profit margins, if any, will surely be lower as well, again dragging down the corporate average.

Now, this is all interesting stuff, but does it matter to anyone who isn't a Marketo investor? Probably not. Spark may push prices a little lower and may put a small crimp in some competitors' growth rates. It may also give small business marketers another fine set of resource materials to complement those from HubSpot and others. But the bottom line is that similar capabilities were already available at a similar price point from Marketo and others. Spark just doesn't change much.

Tuesday, September 13, 2011

Pardot Stays Focused on Small and Mid-Size Clients

I caught up last week with Pardot co-founder and Chief Operating Office Adam Blitzer. It had been over a year since I’d had a serious briefing from Pardot, although we do keep in touch and I have current information on them in my VEST report on industry vendors. Pardot is funny that way: with nearly 700 clients, they’re arguably the third-largest B2B marketing automation vendor and have a broad industry presence, but their formal marketing is relatively quiet. For example, their Web site lists eight press releases during 2011, compared with 46 for Eloqua and 30 for Marketo.

The company’s product strategy takes a similarly modest approach, favoring incremental improvements over bold new directions. The biggest news in its latest release, announced August 31, was using Qwerly to copy public social media profiles into the marketing database. Nice, but not unique: Eloqua, Net-Results and SalesFusion have similar connectors and there are probably others. The new release also included sending pre-scheduled social media messages from within the system and tracking social content consumption and resharing at the individual level. Again, good stuff but not revolutionary.

The previous release, announced last May, also featured a number of small steps, including better tagging of marketing content, more precise control over data synchronization, and a plugin to capture Gmail messages within the Pardot database.

Pardot can limit itself to small refinements because it already provides all the basic marketing automation features. This approach also reflects the company’s disciplined focus on small and mid-size businesses, which don’t want the complexity added by advanced features. Less positively, the modest enhancements may also reflect Pardot’s constrained resources – the company has no outside funding and sells at relatively low prices of $1,000 to $3,000 per month.

This doesn’t mean that Pardot lacks some interesting features. One is an ability to capture the search terms used by individuals, both when they find the company Web site through search engines like Google and when they search within the company site itself. In-site search is a powerful indicator of intent and not one I recall seeing in other marketing automation systems. Pardot also has connectors for SugarCRM, NetSuite, and Microsoft CRM as well as Salesforce.com – not unique, but a broader range than most. The company is adding Webinar integration, starting with Webex and soon to be followed by ReadyTalk.

But features are just part of the equation for marketing automation buyers, especially at small and mid-size businesses. Ease of use, pricing, and support weigh at least as heavily, and Pardot scores well on all three counts. Pardot still uses only inside sales people to keep down its selling expenses, which is one way keep down its prices. Blitzer argues that still lower pricing would require cuts in customer service and support, which he sees as essential to long-term customer success. Of course, other vendors disagree. Maybe there’s no single answer because different approaches will suit different clients. All we can say right now is that Pardot’s approach seems to be working for them.

The company’s product strategy takes a similarly modest approach, favoring incremental improvements over bold new directions. The biggest news in its latest release, announced August 31, was using Qwerly to copy public social media profiles into the marketing database. Nice, but not unique: Eloqua, Net-Results and SalesFusion have similar connectors and there are probably others. The new release also included sending pre-scheduled social media messages from within the system and tracking social content consumption and resharing at the individual level. Again, good stuff but not revolutionary.

The previous release, announced last May, also featured a number of small steps, including better tagging of marketing content, more precise control over data synchronization, and a plugin to capture Gmail messages within the Pardot database.

Pardot can limit itself to small refinements because it already provides all the basic marketing automation features. This approach also reflects the company’s disciplined focus on small and mid-size businesses, which don’t want the complexity added by advanced features. Less positively, the modest enhancements may also reflect Pardot’s constrained resources – the company has no outside funding and sells at relatively low prices of $1,000 to $3,000 per month.

This doesn’t mean that Pardot lacks some interesting features. One is an ability to capture the search terms used by individuals, both when they find the company Web site through search engines like Google and when they search within the company site itself. In-site search is a powerful indicator of intent and not one I recall seeing in other marketing automation systems. Pardot also has connectors for SugarCRM, NetSuite, and Microsoft CRM as well as Salesforce.com – not unique, but a broader range than most. The company is adding Webinar integration, starting with Webex and soon to be followed by ReadyTalk.

But features are just part of the equation for marketing automation buyers, especially at small and mid-size businesses. Ease of use, pricing, and support weigh at least as heavily, and Pardot scores well on all three counts. Pardot still uses only inside sales people to keep down its selling expenses, which is one way keep down its prices. Blitzer argues that still lower pricing would require cuts in customer service and support, which he sees as essential to long-term customer success. Of course, other vendors disagree. Maybe there’s no single answer because different approaches will suit different clients. All we can say right now is that Pardot’s approach seems to be working for them.

Wednesday, June 30, 2010

LoopFuse Offers Free Marketing Automation System: Another Step Towards Industry Consolidation

Summary: LoopFuse has launched a free entry-level version of its marketing automation system. It's one example of how vendors are now competing to attract new users. Only the winners will survive industry consolidation, which may be here sooner than you think.

LoopFuse today promised to “transform” the marketing automation industry by offering a free version of its system. Although LoopFuse and others already provide free trials, this is indeed different: while most free trials expire after 30 days and often have limited functionality, LoopFuse’s FreeView can be used for as long as you like and provides pretty much the same features as the paid version of the system. The critical constraint is that volume is limited to 2,500 prospect names, 5,000 emails and 100,000 page views per month. In practice, this means that only very small companies will actually be able to use the free system as their primary long-term marketing system.

LoopFuse knows that, of course. When they briefed me last week, they said the main purpose of the new system is really to entice trial among companies just starting with marketing automation. They’ll make their money when users see the value they gain and pay for higher volumes and add-on features.

Personally, I’d argue that the really significant news out of LoopFuse is their newly tiered pricing structure. The entry point of $350 per month (for up to 10,000 prospects with unlimited emails and page views) is much lower than the $1,000 to $2,000 starting price of most full-function marketing automation systems. Prices at higher volumes are also much lower than competitors. This will put substantial pricing pressure on vendors who, in many cases, are already struggling to reach sustainable margins.

Here’s where the free system comes back into play. To make a free product viable, LoopFuse needed to engineer as much cost as possible out of the entire client life cycle. This means it had to be possible for clients to purchase and configure the system, learn how to use it and resolve support issues with next to no involvement by LoopFuse staff. Once this was accomplished, LoopFuse was in a position to charge lower fees to its paying clients as well. Other vendors – notably Pardot – have followed a similar cost-removal strategy. But LoopFuse may have been more focused than anyone else.

This doesn’t mean that LoopFuse’s success is guaranteed. Other vendors have similar price points for the small business market (see my list of demand generation vendors) although I suspect their internal costs are higher.

More important, price is just one factor in picking a system. Features, ease of use, and support from the vendor and business partners are usually (and rightly) the main considerations. The free product should increase the number of companies that try LoopFuse first, which will gain it paying customers down the road. But I think that most buyers will recognize that they are likely to stay with their first system and conduct a careful evaluation before they start.

For evidence that a free entry-level product does not automatically drive out higher priced systems, consider the hosted CRM market. Salesforce.com easily dominates despite the presence of surprisingly capable free products like ZohoCRM and FreeCRM .

Whatever the result for LoopFuse, the new offering is part of a larger pattern within the industry. Marketing automation (more precisely, B2B marketing automation) has now passed beyond the pioneer stage where fundamentally different approaches compete for acceptance. At this point, we all pretty much know what a marketing automation system does and, truth be told, the major systems are functionally quite similar.

Competition now shifts from building a technically better system to surviving the inevitable industry consolidation. This requires finding ways to attract masses of new customers as they enter the market.

LoopFuse’s price-driven approach is one such strategy. But many vendors have recently taken others:

- Eloqua, Silverpop, True Influence and at least one other vendor I can’t name are planning new interfaces that they believe will substantially improve ease of use, which they see as the critical barrier blocking many potential buyers. I’m skeptical that truly radical improvements are possible but am certainly eager to see what they come up with.

- LeadLife has embedded best practice hints throughout its system, another way to support adoption by users who lack marketing automation knowledge.

- Infusionsoft has repositioned itself as “email 2.0” rather than marketing automation. They believe this makes it easier for their target customers (under 25 employees) to see them as the next logical step beyond standard email.

- Genius.com added a new Demand Generation edition that falls between its basic Email Marketing and full-blown Marketing Automation products. This is another way of easing the transition from basic email marketing.

- LeadForce1 launched a solution that uses advanced text analysis to measure user intent, and thus provide much better guidance to salespeople than conventional behavioral analysis. Although their approach is based on superior technology, it's still a way to attract customers by offering radically greater value than competitors.

- Marketo now calls itself a “the revenue cycle management company”, giving equal public weight to lead management, sales insight and analytics. They still haven’t briefed me on this or their features to support large enterprises, but they seem to be seeking larger, more sophisticated clients who will presumably provide higher profit margins. Given how many other vendors are targeting small businesses, this certainly makes sense. But Marketo will also find itself competing with established marketing automation vendors like Aprimo, Neolane and Unica. who are entering this market from a different direction. It will also be competing with Eloqua, Silverpop and, perhaps most dangerously, the Market2Lead technology recently purchased by Oracle.

The Market2Lead-Oracle deal raises the other major question facing marketing automation vendors: what role CRM vendors will play? In addition to Oracle, CDC Software (owner of Pivotal CRM and MarketFirst) recently invested in Marketbright.

Of course, the really big question is whether Salesforce.com will make a similar move. There have been off-and-on rumors along those lines for months, followed by stout (if not necessarily credible) denial from Salesforce.com that it has any interest in that direction. I’ve tended to take them at their word, but Oracle and Salesforce.com are blood rivals, so Oracle’s move could easily prompt a Salesforce.com reaction.

Oddly enough, no seems to consider whether Microsoft will enter the game. That's surely a possibility, and would move towards a certainty if its two big on-demand CRM rivals both added marketing automation products. We might even see Google and Intuit participate: both already sell to small business marketers.

My fundamental conclusion is that the B2B marketing automation industry is about to enter the long-predicted stage of vendor consolidation, and that this will move quite quickly. The survivors will serve particular market segments: primarily small vs. large businesses, plus possibly some vertical industry specialization. The window for new entrants is rapidly closing, so any new player will need a major differentiator that creates a clear advantage and distinct identity.

LoopFuse today promised to “transform” the marketing automation industry by offering a free version of its system. Although LoopFuse and others already provide free trials, this is indeed different: while most free trials expire after 30 days and often have limited functionality, LoopFuse’s FreeView can be used for as long as you like and provides pretty much the same features as the paid version of the system. The critical constraint is that volume is limited to 2,500 prospect names, 5,000 emails and 100,000 page views per month. In practice, this means that only very small companies will actually be able to use the free system as their primary long-term marketing system.

LoopFuse knows that, of course. When they briefed me last week, they said the main purpose of the new system is really to entice trial among companies just starting with marketing automation. They’ll make their money when users see the value they gain and pay for higher volumes and add-on features.

Personally, I’d argue that the really significant news out of LoopFuse is their newly tiered pricing structure. The entry point of $350 per month (for up to 10,000 prospects with unlimited emails and page views) is much lower than the $1,000 to $2,000 starting price of most full-function marketing automation systems. Prices at higher volumes are also much lower than competitors. This will put substantial pricing pressure on vendors who, in many cases, are already struggling to reach sustainable margins.

Here’s where the free system comes back into play. To make a free product viable, LoopFuse needed to engineer as much cost as possible out of the entire client life cycle. This means it had to be possible for clients to purchase and configure the system, learn how to use it and resolve support issues with next to no involvement by LoopFuse staff. Once this was accomplished, LoopFuse was in a position to charge lower fees to its paying clients as well. Other vendors – notably Pardot – have followed a similar cost-removal strategy. But LoopFuse may have been more focused than anyone else.

This doesn’t mean that LoopFuse’s success is guaranteed. Other vendors have similar price points for the small business market (see my list of demand generation vendors) although I suspect their internal costs are higher.

More important, price is just one factor in picking a system. Features, ease of use, and support from the vendor and business partners are usually (and rightly) the main considerations. The free product should increase the number of companies that try LoopFuse first, which will gain it paying customers down the road. But I think that most buyers will recognize that they are likely to stay with their first system and conduct a careful evaluation before they start.

For evidence that a free entry-level product does not automatically drive out higher priced systems, consider the hosted CRM market. Salesforce.com easily dominates despite the presence of surprisingly capable free products like ZohoCRM and FreeCRM .

Whatever the result for LoopFuse, the new offering is part of a larger pattern within the industry. Marketing automation (more precisely, B2B marketing automation) has now passed beyond the pioneer stage where fundamentally different approaches compete for acceptance. At this point, we all pretty much know what a marketing automation system does and, truth be told, the major systems are functionally quite similar.

Competition now shifts from building a technically better system to surviving the inevitable industry consolidation. This requires finding ways to attract masses of new customers as they enter the market.

LoopFuse’s price-driven approach is one such strategy. But many vendors have recently taken others:

- Eloqua, Silverpop, True Influence and at least one other vendor I can’t name are planning new interfaces that they believe will substantially improve ease of use, which they see as the critical barrier blocking many potential buyers. I’m skeptical that truly radical improvements are possible but am certainly eager to see what they come up with.

- LeadLife has embedded best practice hints throughout its system, another way to support adoption by users who lack marketing automation knowledge.

- Infusionsoft has repositioned itself as “email 2.0” rather than marketing automation. They believe this makes it easier for their target customers (under 25 employees) to see them as the next logical step beyond standard email.

- Genius.com added a new Demand Generation edition that falls between its basic Email Marketing and full-blown Marketing Automation products. This is another way of easing the transition from basic email marketing.

- LeadForce1 launched a solution that uses advanced text analysis to measure user intent, and thus provide much better guidance to salespeople than conventional behavioral analysis. Although their approach is based on superior technology, it's still a way to attract customers by offering radically greater value than competitors.

- Marketo now calls itself a “the revenue cycle management company”, giving equal public weight to lead management, sales insight and analytics. They still haven’t briefed me on this or their features to support large enterprises, but they seem to be seeking larger, more sophisticated clients who will presumably provide higher profit margins. Given how many other vendors are targeting small businesses, this certainly makes sense. But Marketo will also find itself competing with established marketing automation vendors like Aprimo, Neolane and Unica. who are entering this market from a different direction. It will also be competing with Eloqua, Silverpop and, perhaps most dangerously, the Market2Lead technology recently purchased by Oracle.

The Market2Lead-Oracle deal raises the other major question facing marketing automation vendors: what role CRM vendors will play? In addition to Oracle, CDC Software (owner of Pivotal CRM and MarketFirst) recently invested in Marketbright.

Of course, the really big question is whether Salesforce.com will make a similar move. There have been off-and-on rumors along those lines for months, followed by stout (if not necessarily credible) denial from Salesforce.com that it has any interest in that direction. I’ve tended to take them at their word, but Oracle and Salesforce.com are blood rivals, so Oracle’s move could easily prompt a Salesforce.com reaction.

Oddly enough, no seems to consider whether Microsoft will enter the game. That's surely a possibility, and would move towards a certainty if its two big on-demand CRM rivals both added marketing automation products. We might even see Google and Intuit participate: both already sell to small business marketers.

My fundamental conclusion is that the B2B marketing automation industry is about to enter the long-predicted stage of vendor consolidation, and that this will move quite quickly. The survivors will serve particular market segments: primarily small vs. large businesses, plus possibly some vertical industry specialization. The window for new entrants is rapidly closing, so any new player will need a major differentiator that creates a clear advantage and distinct identity.

Wednesday, December 03, 2008

Pardot Offers Refined Demand Generation at a Small Business Price

My little tour of demand generation vendors landed at Pardot just before Thanksgiving. As you’ll recall from my post on Web activity statistics, Pardot is one of the higher-ranked vendors not already in the Raab Guide to Demand Generation Systems. So I was quite curious to see what they had to offer.

What I found was intriguing. While last week’s post found that Marketbright aims at more sophisticated clients, Pardot explicitly targets small and midsize businesses (or SMBs as we fondly acronymize them [yes, that’s a word, at least according to http://www.urbandictionary.com/]). Actually I don’t know why I find the contrast between Pardot and Marketbright intriguing, except for the implication that marketers can be divided into two simple categories, SMB and Enterprise, and no further distinctions are necessary. The analyst in me rejects this as an obvious and appalling over-simplification, but there’s a sneaky, almost guilty pleasure in contemplating whether it might be correct.

What’s odd about the SMB vs. Enterprise dichotomy is that both sets of systems are quite similar. Pardot and other SMB systems don’t just offer a few simple features. In fact, Pardot in particular provides advanced capabilities including progressive profiling (automatically changing the questions on forms as customer answer them) and dynamic content (rule-driven selection of content blocks within emails and Web pages). The only common feature that’s missing in Pardot is rule-based branching within multi-step programs. Even this is far from a fatal flaw, since (a) users can simulate it with rules that move customers from one program to another and (b) intra-program branching will be added by the end of this month.

What really distinguishes the Enterprise vendors is the ability to limit different users to different tasks. This involves rights management and content management features that seem arcane but are nevertheless critical when marketing responsibilities are divided by function, channel, region and product organizations. Although enterprise marketing programs are more complex than SMB programs, most SMB systems can actually handle complex programs quite well. Conversely, although SMB vendors stress their products’ ease of use, simple things are not necessarily harder to do in the Enterprise products. I’m still trying to work out a systematic approach to measuring usability, but my current feeling is that there are large variations among products with both the SMB and Enterprise groups.

Back to Pardot. It certainly considers ease of use to be one of its advantages, and I saw nothing to contradict this. Functionally, it has all the capabilities you’d expect of a demand generation product: users create personalized emails and Web pages with a drag-and-drop interface; track responders with cookies; look up visitors' companies based on their IP address; run multi-step drip marketing campaigns; score leads based on activities and attributes; and integrate tightly with Salesforce.com and other CRM systems. These are nicely implemented with refinements including:

- integrated site search, including the ability to use visitor queries as part of their behavior profiles (something I haven’t seen in other demand generation products)

- different scoring rules for customers in different segments (other systems could achieve this but not so directly)

- auto-response messages tied to completion of an email form (again, this often requires more work in other systems)

- ability to post data from externally-hosted forms via API calls (not just batch file imports) and to forward posted data to external systems

- email address validation that goes beyond the format checking available in most products to include rejecting addresses from free domains such as gmail or yahoo, and validating that the address is active on the specified host

- ability to capture campaign costs by importing data from Google AdWords and other sources

- plug-ins that let the system track emails sent by Outlook, Thunderbird and Apple email clients

This is an impressive list that suggests a thoughtfully designed system. But I didn’t check Pardot against my full list of possible features, so don’t get the impression that it does everything. For example, its approach to revenue reporting is no better than average: the system imports revenue from the sales automation opportunity records, and then assigns it to the first campaign of the associated lead. This is a common approach, but quite simplistic. More sophisticated methods give more control over which campaigns are credited and can divide revenue among multiple campaigns. Nor does Pardot have the refined user rights management and content management features associated with enterprise systems. It also limits database customization to adding user-defined fields to the prospect table. (This is another area where Enterprise vendors tend to be more flexible than SMB systems, albeit with considerable variation within each group.)

The point here is that Pardot, like all systems, has its own strengths and weaknesses. This is why the simple SMB vs. Enterprise dichotomy isn’t enough. People who need specific features won’t necessarily find them in all products of one group or the other. You really do have to look closely at the individual products before making a choice. QED.

One other factor clearly distinguishes SMB from Enterprise systems, and that’s pricing. Pardot’s lowest-price system, $500 per month, may be too constrained for most companies (no CRM integration, maximum of five landing pages, etc.),. But its $750 per month offering should be practical for many SMBs and a $1,250 per month option allows still higher volumes. (Pricing details are published on their Web site – which is itself typical of SMB products.) This pricing is low even among SMB demand generation systems. By comparison, limited versions cost $1,500 per month for Marketo and $1,000 for Manticore Technology, and both charge $2,400 per month for their cheapest complete offering. (Note: other SMB-oriented vendors including ActiveConversion and OfficeAutoPilot also have entry pricing in the $500 per month range, although neither publishes the details.)

The Pardot product began as an internal project for the marketing group at Hannon Hill, a content management system developer. Pardot was spun off about two years ago and launched its product at the end of 2007. It recently signed its 100th client.

Wednesday, November 19, 2008

Ranking the Demand Generation Vendors by Popularity (Yes, Life Really Is Just Like High School)

As you might imagine, I’ve been trying to decide how to expand the set of products covered in the Raab Guide to Demand Generation Systems. My original plan had been to add several marketing automation vendors with significant presence in this market. The tentative list is Unica, Aprimo, Alterian, and Neolane.

But I’ve also been approached by some of the other demand generation specialists. My original set of products was based on a general knowledge of which companies are most established, plus some consultation with vendors to learn who they felt were their main competitors. So far the original list of Eloqua, Vtrenz, Marketo, Manticore Technology and Market2Lead has proven a good set of choices. Yet there are so many more vendors I could add. How to choose?

The general rule is pretty obvious: pick the vendors that people are most interested in. We do, after all, want people to buy this thing. Of course, you want some wiggle room to add intriguing new products that they may not know about. Still, you mostly want to the report to include the vendors they are already asking about.

But although the general rule is obvious, which vendors are most popular is not. Fortunately, we have the Internet to help. It offers quite a few ways to measure interest in a vendor: Web searches, blog mentions, Google hits, and site traffic among them. All are publicly available with almost no effort. After a close analysis of the alternatives, I have decided the Alexa.com traffic statistics are the best indicator of vendor market presence. (You can read about the analysis in fascinating detail on my marketing measurement blog, MPM Toolkit.)

The table below shows the Alexa rankings and share statistics for the current Guide entries, the four marketing automation vendors already mentioned, and a dozen or so contenders.

The figures themselves need a little explaining. The Alexa rank is a “combined measure of page views and number of users”, with the most popular site ranked number 1, next-most-popular ranked number 2, etc. (In case you're wondering, the top three are Yahoo!, Google and YouTube.) Alexa share represents “percent of global Internet users who visit this site”. The rank and share figures correlate closely, but share is probably for comparing sites, since the ratio directly reflects relative traffic. That is, a share figure twice as large as another share figure indicates twice as many visitors, while a rank that is one half as large as another rank doesn’t necessarily mean twice as much traffic.

The figures for the existing vendors, in the first block of the table, give pretty much the ranking you’d expect. One wrinkle is that Vtrenz is owned by Silverpop, so Silverpop.com presumably siphons off a great deal of traffic from Vtrenz.com. On the other hand, Silverpop is a major email service provider in its own right, so a large share of the Silverpop.com traffic probably has nothing to do with Vtrenz. In any event, I’ve listed both sites in the table. Vtrenz is clearly a major vendor, so nothing is at stake here except bragging rights.

What’s more interesting is the figures for the Marketing Automation group. Unica is quite popular, while the other vendors are much less visited. This doesn’t particularly surprise me, although seeing Alterian, Aprimo and Neolane rank well below Manticore Technology and Market2Lead is odd. Perhaps these vendors are more obscure than I had realized. Still, they are much larger firms and do much more marketing than Manticore or Market2Lead. Interestingly, the other measure I found somewhat credible, IceRocket’s count of blog mentions, ranks Alterian, Aprimo and Neolane considerably higher than Manticore and Market2Lead. (See the MPM Toolkit post for details.) So the marketing automation vendors are probably a little more important to potential Guide buyers than the Alexa numbers suggest.

But my real concern was the Other Demand Generation group. Here, the Alexa figures do provide some very helpful insights. Basically they suggest that Marketbright, Pardot, Marqui and ActiveConversion, are all pretty much comparable in market presence to Manticore and Market2Lead. I spoke with Marketbright and Pardot this week and connected with ActiveConversion some time ago. Based on those conversations, this seems about right. (Marqui is a special case because they fell on financial hard times and the assets were recently purchased.) Rankings fall off sharply for the other vendors on the list, providing a reasonable cut-off point for the next round of Guide entries.

Of course, nothing is set in stone. Perhaps one of the smaller vendors can convince me that they have something special enough to justify including them. Plus there is still the question of whether I should invest the effort to expand the Guide at all, and what sequence I do the additions. But, whatever the final result, it’s nice to have an objective way to measure vendor market presence.

But I’ve also been approached by some of the other demand generation specialists. My original set of products was based on a general knowledge of which companies are most established, plus some consultation with vendors to learn who they felt were their main competitors. So far the original list of Eloqua, Vtrenz, Marketo, Manticore Technology and Market2Lead has proven a good set of choices. Yet there are so many more vendors I could add. How to choose?

The general rule is pretty obvious: pick the vendors that people are most interested in. We do, after all, want people to buy this thing. Of course, you want some wiggle room to add intriguing new products that they may not know about. Still, you mostly want to the report to include the vendors they are already asking about.

But although the general rule is obvious, which vendors are most popular is not. Fortunately, we have the Internet to help. It offers quite a few ways to measure interest in a vendor: Web searches, blog mentions, Google hits, and site traffic among them. All are publicly available with almost no effort. After a close analysis of the alternatives, I have decided the Alexa.com traffic statistics are the best indicator of vendor market presence. (You can read about the analysis in fascinating detail on my marketing measurement blog, MPM Toolkit.)

The table below shows the Alexa rankings and share statistics for the current Guide entries, the four marketing automation vendors already mentioned, and a dozen or so contenders.

Alexa | Alexa | |

rank | share | |

Already in Guide: | ||

| Eloqua | 20,234 | 0.007070 |

| Silverpop | 29,080 | 0.003050 |

| Marketo | 68,088 | 0.001700 |

| Manticore Technology | 213,546 | 0.000610 |

| Market2Lead | 235,244 | 0.000480 |

| Vtrenz | 295,636 | 0.000360 |

Marketing Automation: | ||

| Unica / Affinium* | 126,215 | 0.000850 |

| Alterian | 345,543 | 0.000250 |

| Aprimo | 416,446 | 0.000220 |

| Neolane | 566,977 | 0.000169 |

| Other Demand Generation: | ||

| Marketbright | 167,306 | 0.000540 |

| Pardot | 211,309 | 0.000360 |

| Marqui Software | 211,767 | 0.000440 |

| ActiveConversion | 257,058 | 0.000340 |

| Bulldog Solutions | 338,337 | 0.000320 |

| OfficeAutoPilot | 509,868 | 0.000200 |

| Lead Genesys | 557,199 | 0.000145 |

| LoopFuse | 734,098 | 0.000109 |

| eTrigue | 1,510,207 | 0.000043 |

| PredictiveResponse | 2,313,880 | 0.000033 |

| FirstWave Technologies | 2,872,765 | 0.000017 |

| NurtureMyLeads | 4,157,304 | 0.000014 |

| Customer Portfolios | 5,097,525 | 0.000009 |

| Conversen* | 6,062,462 | 0.000007 |

| FirstReef | 11,688,817 | 0.000001 |

The figures themselves need a little explaining. The Alexa rank is a “combined measure of page views and number of users”, with the most popular site ranked number 1, next-most-popular ranked number 2, etc. (In case you're wondering, the top three are Yahoo!, Google and YouTube.) Alexa share represents “percent of global Internet users who visit this site”. The rank and share figures correlate closely, but share is probably for comparing sites, since the ratio directly reflects relative traffic. That is, a share figure twice as large as another share figure indicates twice as many visitors, while a rank that is one half as large as another rank doesn’t necessarily mean twice as much traffic.

The figures for the existing vendors, in the first block of the table, give pretty much the ranking you’d expect. One wrinkle is that Vtrenz is owned by Silverpop, so Silverpop.com presumably siphons off a great deal of traffic from Vtrenz.com. On the other hand, Silverpop is a major email service provider in its own right, so a large share of the Silverpop.com traffic probably has nothing to do with Vtrenz. In any event, I’ve listed both sites in the table. Vtrenz is clearly a major vendor, so nothing is at stake here except bragging rights.

What’s more interesting is the figures for the Marketing Automation group. Unica is quite popular, while the other vendors are much less visited. This doesn’t particularly surprise me, although seeing Alterian, Aprimo and Neolane rank well below Manticore Technology and Market2Lead is odd. Perhaps these vendors are more obscure than I had realized. Still, they are much larger firms and do much more marketing than Manticore or Market2Lead. Interestingly, the other measure I found somewhat credible, IceRocket’s count of blog mentions, ranks Alterian, Aprimo and Neolane considerably higher than Manticore and Market2Lead. (See the MPM Toolkit post for details.) So the marketing automation vendors are probably a little more important to potential Guide buyers than the Alexa numbers suggest.

But my real concern was the Other Demand Generation group. Here, the Alexa figures do provide some very helpful insights. Basically they suggest that Marketbright, Pardot, Marqui and ActiveConversion, are all pretty much comparable in market presence to Manticore and Market2Lead. I spoke with Marketbright and Pardot this week and connected with ActiveConversion some time ago. Based on those conversations, this seems about right. (Marqui is a special case because they fell on financial hard times and the assets were recently purchased.) Rankings fall off sharply for the other vendors on the list, providing a reasonable cut-off point for the next round of Guide entries.

Of course, nothing is set in stone. Perhaps one of the smaller vendors can convince me that they have something special enough to justify including them. Plus there is still the question of whether I should invest the effort to expand the Guide at all, and what sequence I do the additions. But, whatever the final result, it’s nice to have an objective way to measure vendor market presence.

Subscribe to:

Comments (Atom)